In the dawn of 2025, a leading alternative investment manager announced the launch of an US $450 million private credit fund – its third since 2017. This will be lent in the seven-year tenure space with ticket sizes US $20million to US $50million. This momentum continued within 2025. Global and local pools of capital are finding investment avenues. Another transaction in the private credit sector has resulted when three private credit funds - Kotak Special Situation Fund, an Edelweiss Special Opportunities Fund and Allianz Global Investors - agreed to jointly provide a ?3,200 crore debt facility to steel maker Jayaswal Neco (the company used the funds to repay high-cost money raised from the Ares SSG-backed Assets Care and Reconstruction Enterprise (ACRE)).

SARFAESI and IBC Act are two mechanisms that help India’s financial services market to rationalize the foreclosure processes, while it could be an opportunity to transform distressed assets to sustainable investment opportunities. The IBC Act, 2016 have created a wide array of investment opportunities for private credit lenders. This Regulatory reform created restrictions on banks to financing a series of end uses – i.e.: share acquisition, land acquisition, equity investments, etc… All these types of investments can be now pursued by alternative lenders at a higher cost of capital that in some cases led to non-performing assets/loans, and distressed situations or even in bankruptcies.

IBC Act and Bankruptcies

India’s bankruptcy filings have been tracked by the Insolvency and Bankruptcy Board of India (IBBI) since the IBC’s inception. Year-wise filings exceeded 1,700 per year between 2019–2023 for companies but fell in volume post-pandemic due to moratoriums and regulatory changes (

Search | Open Government Data (OGD) Platform India).

India's insolvency/distressed assets investment market is estimated at around USD 10 billion (2024), primarily reflecting private credit and asset resolution deals rather than court filings alone. With the resolution regime strengthening, private credit/distressed assets market is projected to grow above 10% CAGR, reaching USD 16–18 billion by 2027 (according to a recent report by PwC India). In addition, there is an adjacent market of bankruptcy software and services (i.e. insolvency management platforms) that has a size of US $173mn (2024), forecasted to reach US $456mn by 2033. India’s debt collection software market is expanding due to rising digital adoption, AI-driven automation, and regulatory compliance demands. Businesses are integrating predictive analytics, mobile-friendly interfaces, and secure data management to enhance recovery efficiency, reduce operational costs, and ensure transparency in debt collection processes, according to imarc’s report.

The Insolvency and Bankruptcy Code (IBC) provide an effective resolution tool for alternative asset managers – for instance, private credit lenders/AIFs cannot use the Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest (SARFAESI) Act of 2002 to settle their dues without court intervention like traditional lenders. They can, however, use IBC for recoveries. the Corporate Insolvency Resolution Process (CIRP) is targeted to be completed within a period of 11 months (on average), including the litigation time.

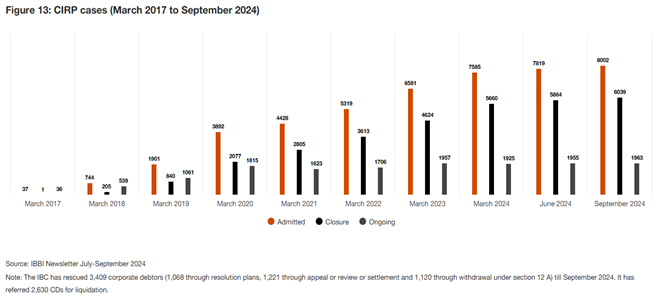

CIRP cases (March 2017 to September 2024)

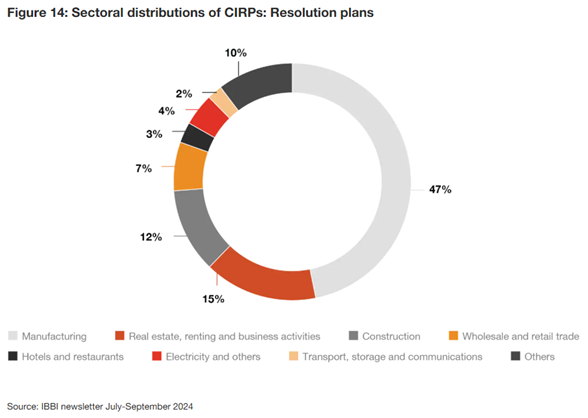

A recent newsletter by the IBBI (July-September 2024) , shows that the vast majority of the Corporate Insolvency Resolutions are coming from the manufacturing sector (47%), with real estate (15%) and construction (12%) to follow, a trend which shows there could be plenty of real assets that can be acquired and live a new life after a proper asset repurposing, and following the international trend and need for sustainable development. With the resolution regime strengthening, private credit/distressed assets market is projected to grow above 10% CAGR, reaching USD 16–18 billion by 2027 (

according to study published by PwC India).

Sectoral distributions of Corporate Insolvency Resolutions

SARFAESI and Non-Performing Assets (NPA)

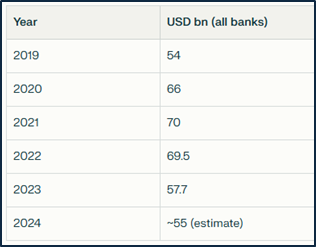

India’s NPA total market size (private banks, public banks, NBFCs) was approx. US $55 billion as of March 2024. Public sector bank net NPAs dropped sharply from 2.8 trillion INR (2019) to 725 billion INR (2024), or about US $8.7 billion. The Non-Performing Loans (NPL) management services market was USD 3 billion in 2024, projected to reach USD 7.1 billion by 2027 at a 57% CAGR. In addition, as loan quality improves, headline NPA stock is expected to remain roughly constant in dollar terms, but the addressable distressed asset market (incl. resolutions, sales, recoveries) will grow.

Total NPAs (in USD billion, end of March for each year)

For the period FY22–23, banks and NBFCs invoked SARFAESI for thousands of loans annually, with cumulative asset values in the tens of billions USD. The Act remains the key non-judicial recovery tool for secured loans, especially in real estate and large corporates. Recent amendments, fast-tracked the possession and sales, and inclusion of NBFCs, and this increased SARFAESI adoption for stressed asset resolution.

Public data lists high value of assets under attempted enforcement but does not publish a consolidated USD value annually for SARFAESI actions. The recent regulatory reforms, the new creditor-initiated insolvency (2025 Bill), economic normalization, and digital transformation are expected to expand the formal distressed assets market.

Analysts expect a compounded growth in both value and volume of distressed assets resolved via IBC and SARFAESI, with incoming private capital and asset sales likely surpassing USD 16–18 billion by 2027.

Insolvency/Distressed assets and debt (IBC) as well as non-performance assets (SARFAESI) are two adjacent markets with different attributes and characteristics. Business insolvencies are expected to stabilize and marginally rise the coming years due to global uncertainties and the local regulatory framework. Distressed debt is expected to rise fuelled by the RBI rules that allow securitization of distressed assets, and inflows from foreign funds, while asset reconstruction activity is projected to steadily grow, with the formal insolvency ecosystem maturing, improving transparency, and shortening resolution duration. Lastly, gross NPA ratios forecasted to rise slightly for India’s commercial banks: from 2.3% in March 2025 to 2.5% by March 2027, well below previous decade highs and within safe systemic limits. Adverse scenarios (if growth slows or external shocks rise) could push these ratios higher, up to 5.6% in the most severe case. Expansion of bad loan securitization (junk debt) is expected to improve balance sheet health and attract more international investors, expanding the overall distressed asset pool.

To conclude, the structural reforms and regulatory clarity (in IBC, asset reconstruction, and SARFAESI) should continue to drive market sophistication and depth. This market potential is set for significant expansion especially for distressed asset acquisition, ARCs, and securitization, with rising participation from global investors.

ILO Consulting along with our partners, Terra Pivot Capital have the prior experience from similar local transactions and the international access to the appropriate funding to efficiently manage the execution of this type of transactions.